Morgan Stanley: Here Are The 4 "Worries" That Will Dominate The Next 6-12 Months

By Andrew Sheets, Chief Cross-Asset Strategist for Morgan Stanley

All Gas, No Brakes

The weather in London this week has been rainy while sunny, which feels like a fair description of current sentiment, as we’ve been discussing our mid-year outlook with investors this week. There’s a wide range of views out there at the moment, with the noisiness of the data giving everyone something to hang their hat on. In short, it’s the perfect time to step back and debate the longer-term outlook.

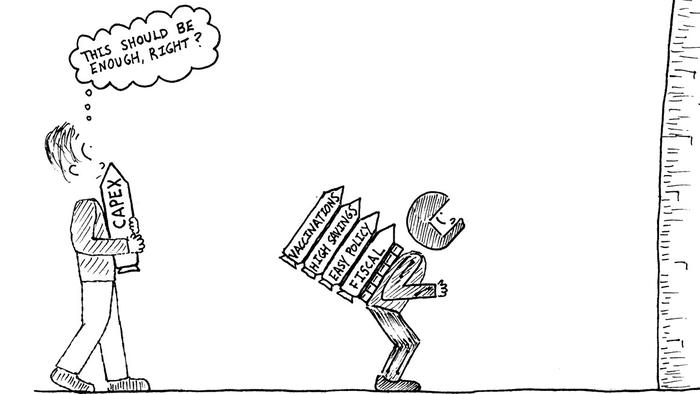

The most notable aspect of our forecasts, and one of the most contentious areas of debate, is just how much our expectations differ from the prior decade. The post-GFC period was defined by fiscal austerity, low investment, a deleveraging consumer and central banks acting pre-emptively to choke off inflationary risk. Indeed, for all that we associate ‘easy policy’ with the last cycle, the PBOC tightening in 2010, the ECB hiking in 2011 and the Fed hiking in 2015 were all aggressive early moves to nip inflation in the bud.

Our expectations this time around couldn’t be more different. Fiscal policy is historically expansionary. The consumer in the US, Europe and China is in outstanding shape, with record levels of savings. We see a ‘red-hot capex cycle’ and public and private sector investment increasing. Global real rates are still near all-time lows. As my colleague Chetan Ahya noted in last week’s Sunday Start, fiscal easing, cheap money, a strong consumer and more investment are four powerful cylinders in the proverbial economic engine.

But just as notable is the expected policy response. In the face of strong growth, we think that central banks remain unusually standoffish. For the Fed, it’s a focus on still-elevated unemployment, coupled with a recent commitment to average inflation targeting. For the ECB, it’s awareness of a long-running inflation undershoot and memories of the 2011 hikes. For China, it’s taking a more gradual approach to tightening than after the last downturn.

In short, it’s a global economy with a lot of gas and few brakes: And if that is so, it means the risk case is different. After a decade where risk often skewed to the downside and the question was what new form of easing would central banks conjure up to fight weakness, the issue now is that growth is good. Hence:

*

Will the recovery create inflation?

*

Will it alter central bank policy?

*

Will that lead to margin and tax pressures?

*

And is good growth already in the price?

If these are the ‘worries’ that will dominate the next 6-12 months, they won’t apply evenly. For US equities and credit, as well as segments of EM, these concerns will be front and center. But for Europe (and Japan), the questions of excessive valuations, high inflation, a hawkish policy shift or new corporate taxes seem much more distant. Maybe this distinction is obvious, but we think that it still works to Europe’s advantage.

A hotter cycle could also mean a shorter cycle, and an unusually fast normalization of conditions. Such a scenario disadvantages credit. The asset class sees outstanding early-cycle, post-recession performance as growth recovers and companies focus on survival. But as things heat up, extra growth doesn’t mean any extra income from a corporate bond. On a cross-asset basis, credit underperforms on our new 12-month forecasts, and credit risk premiums look rich relative to other assets. With a change in view from Srikanth Sankaran and our credit strategy team, we’ve downgraded credit to equal-weight.

Finally, these forecasts invite an even more important structural question. Again, our expectations for strong fiscal, monetary and capital spending and consumer trends are very different from what prevailed over the last decade. Will this mean an exit from the secular stagnation of the post-GFC mindset? If we are right, this should be an increasingly important debate.

As we’ve told this story over the last week, opinions, like the weather, have been mixed. We’ve talked to plenty of investors who think it’s finally Europe’s time to shine, and plenty of others who worry it will remain a serial disappointment. One investor described our expectation that the Fed doesn’t hike until 3Q23 as ‘what the Fed wants to do, not what it will do’, while another thought the Fed wouldn’t be able to complete tapering, given market sensitivity to real rates.

Opinion on the big picture is similarly divided. Indeed, the current debate reminds me quite a bit of 2010, when there was a sharp division between those who expected a rapid return of pre-crisis conditions (higher rates, EM leadership), and those who thought otherwise. As growth and inflation pick up, we expect a trickier summer, but also an ongoing debate around these larger issues. Rain during sunshine could be something we need to get used to. Tyler Durden Sun, 05/23/2021 - 16:30

http://dlvr.it/S0GGKd

No comments:

Post a Comment