Outside Of Tech, There Has Been Zero EPS Growth In The Past 12 Years Tyler Durden Sun, 10/18/2020 - 13:15

By now every professional trader, veteran 16-year-old Robinhooder and mere daytrading amateur - and certainly every value investor left - has seen some version of the following chart, which shows the unprecedented underperformance of value stocks compared to growth.

Analysts have tried hard to explain this divergence, with two main reasons emerging as the cause:

1. The secular decline in bond yields and inflation expectations has boosted the value of longer-duration Growth companies (while hitting Value companies most atrisk of deflation).

As Goldman's Peter Oppenheimer chimes in, the global secular decline in bonds yields started at the peak of inflation in the 1980s and has resulted in remarkable returns in bond markets ever since then. However, it is the declines since the start of this century, in the aftermath of the technology bubble, and even more so after the financial crisis of 2008 - when the Fed launched ZIRP and QE - that have had the most dramatic impact on factor leadership within equities. Indeed, it may be hard to imagine now, but on the eve of the financial crisis in 2008, 10-year Treasury yields and Bund yields were around 4%. Many people at the time thought that these yields were too low. Everyone knows what has happened since then: Bund yields hit a record low of -0.9% and 25% of global debt having a negative yield. As the next chart shows, this has also resulted in global bond yields tumbling to their lowest levels in history, going back to the 1300s.

2. A secular decline in long-term growth expectations, together with greater uncertainty about growth.

Long-term growth expectations have collapsed since the financial crisis both for trend GDP growth and for long-term profit growth: the Goldman chart below shows the long slowdown in consensus real GDP growth 6-10 years forward in all major regions (inverse to the furious accumulation of global debt). And with lower inflation, revenue growth has also slowed materially in the US and Europe, and has approached the kind of growth rates that Japan has experienced over the past couple of decades. Slower growth means that companies that are perceived to be able to achieve growth are considered more valuable, and all the more so given the collapse in the risk free rate.

The market has rewarded growth appropriately: the next chart shows the P/Es of US and European companies in different bands of expected future sales growth. While this tends to be upward sloping (investors are prepared to pay more for higher growth), it has become steeper now than we have tended to see on average in the past. In other words, investors are paying (much) more now for higher expected growth, especially safe top-line growth. Or, as Goldman puts, it, the scarcity of growth means that investors are prepared to pay a big premium for stable secure growth in the few areas that offer it.

But while record low rates and Japanification of growth and inflation - both of which have been caused by central banks we should point out - are certainly credible explanations for the devastation within value stocks, there is a far simpler reason why tech (i.e. growth) has outperformed everything else: earnings growth.

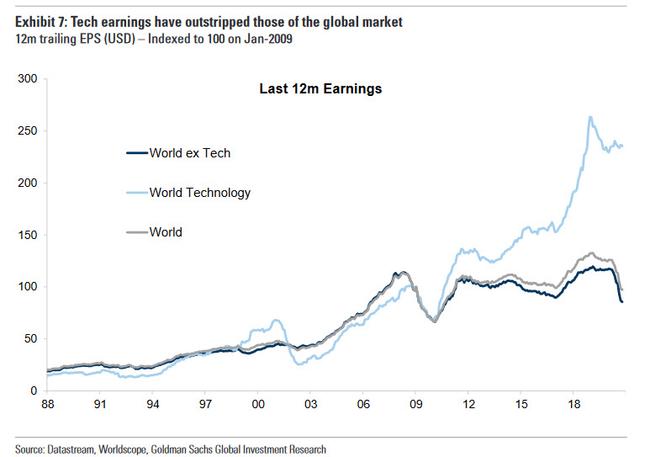

And here is the remarkable punchline: looking back several decades, one can see an unprecedented divergence emerging just after the financial crisis between Technology ROE and EPS... and everyone else. As the final chart shows, if one strips away global tech companies, the World ex-Technology has achieved zero earnings growth since the 2008 crisis.

Which, needless to say, is staggering: it means that the roughly 2000 points of S&P growth since the last crash has been entirely on the back of tech. It also means that the mean-reversion, once it comes as inflation makes its triumphal return (and central bank plans to flood the world with digital currencies in a historic overhaul of the fiat system in the coming years will achieve that virtually overnight) will be historic.

http://dlvr.it/RjrqV2

No comments:

Post a Comment