China's "National Team" Is Good At Killing Stock Volatility

By Ye Xie, Bloomberg Markets Live strategist and commentator

Chinese state-backed funds reportedly intervened in the stock market on Tuesday, helping stem the biggest intraday loss since August 2021.

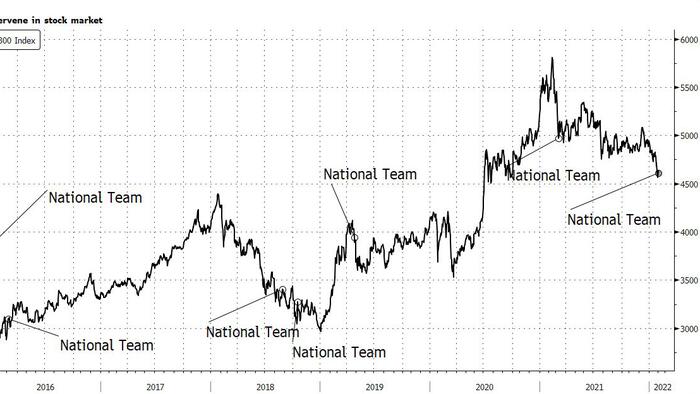

Since the bursting of the stock bubble in 2015, Bloomberg has reported at least seven occasions when the so-called “national team” came to the rescue when the market was cratering. The efforts didn’t always stop the bleeding immediately. But what they are good at is smothering volatility, which may be the very purpose of the intervention.

State-related funds stepped into the market to buy local shares Tuesday afternoon, after the benchmark CSI 300 index slumped 2.4%, Bloomberg reported, citing people with direct knowledge. Shares of financial firms, including brokerages, were among those purchased. The CSI has lost about 7% this year, disappointing investors who had expected policy stimulus would boost stocks.

The most-recent prior appearance of the “national team” occurred in March 2021, when the surge in U.S. yields hammered some highly-valued Chinese stocks during the National People’s Congress. They also intervened during the U.S.-China trade war in 2018 and 2019, and in 2016 in the aftermath of the stock crash.

How effective is the national team’s rescue? On average, stocks continued to decline over the next three months, but at a slower pace. The CSI 300 fell by an average of 2.3% in the month after the reported intervention, compared with a loss of 5.1% in the previous month. The stock market did fare better over the ensuing six-month period, returning 5.5% on average.

What’s more compelling is that the intervention consistently reduced market swings. State funds typically came in when 10-day volatility surged above at least 20. On average, volatility jumped by 9 points a month before the intervention, and declined by almost 14 points in the following month.

In addition to volatility, there could be other clues to predict when the national team may step in. The recent episodes were related to external factors, such as tariff announcements in August 2018. On a few occasions, there seems to have been coordinated efforts by state media to talk up markets before the official intervention, although there have been plenty of false alarms. For instance, two weeks ago, state papers, including Shanghai Securities Journal, called for investors not to overreact to the market decline, saying A-shares have solid support from policies and fund flows.

The old adage is don’t fight the central bank. In China’s context, it’s don’t fight the national team when they want to kill volatility.

Tyler Durden

Tue, 02/08/2022 - 20:05

http://dlvr.it/SJdRrS

No comments:

Post a Comment